There’s a rumor circulating that the emblematic “American Dream” is of little interest to Millennials. Yet, half of all home buyers today are under the age of 36. Renting may not be the new “lifestyle choice” that many analysts and economists have painted it out to be. For many renters, homeownership is still the dream – but not without its financial obstructions.

According to the 2016 Zillow Group Report on Consumer Housing Trends, over half (58 percent) of all renters in the market for a new rental home are also considering buying a home. Nineteen percent are seriously looking to buy and 39 percent “casually consider” homeownership. Millennials and members of Generation X contemplate home buying at the highest rates: 63 percent and 59 percent, respectively.

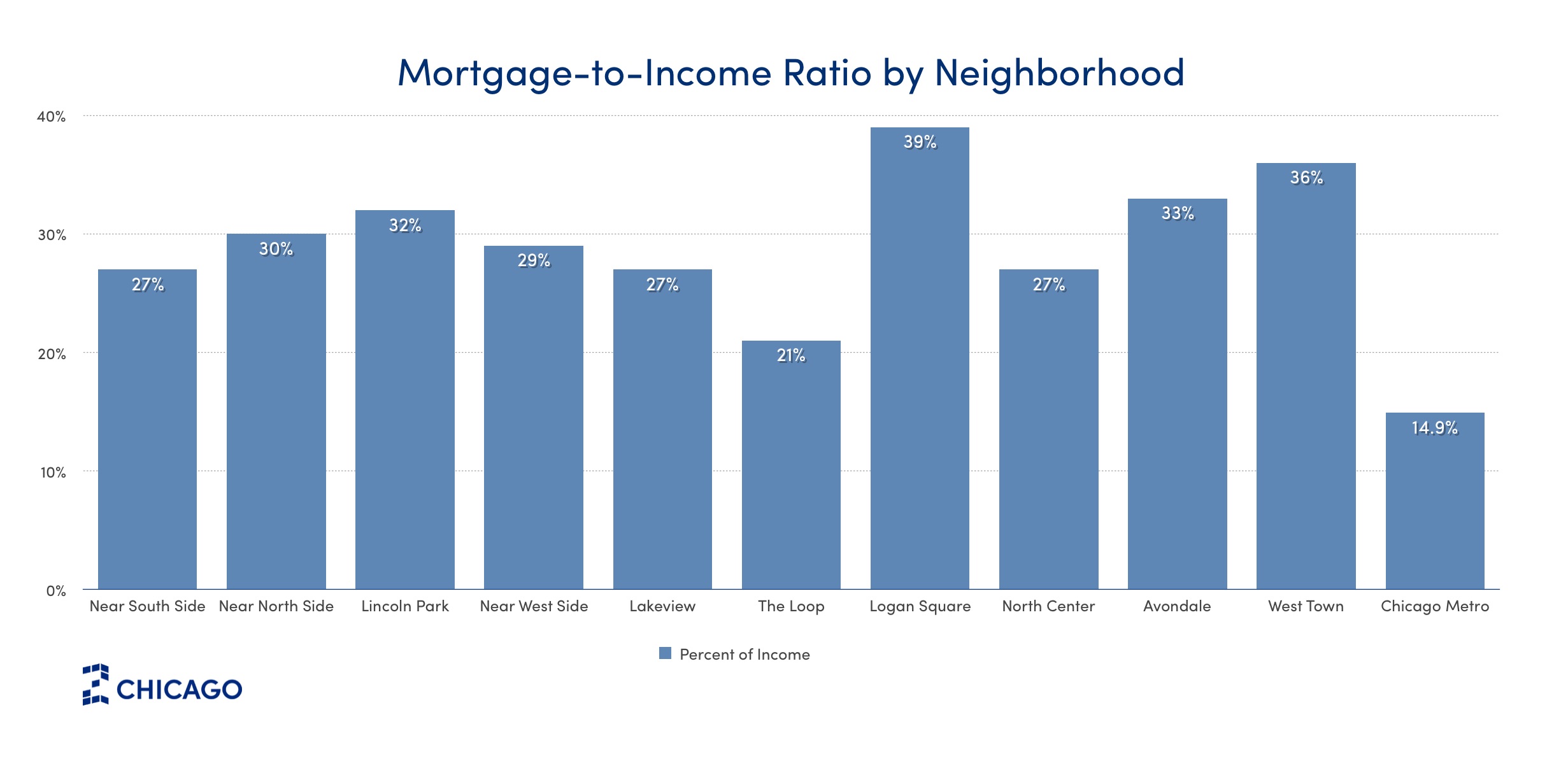

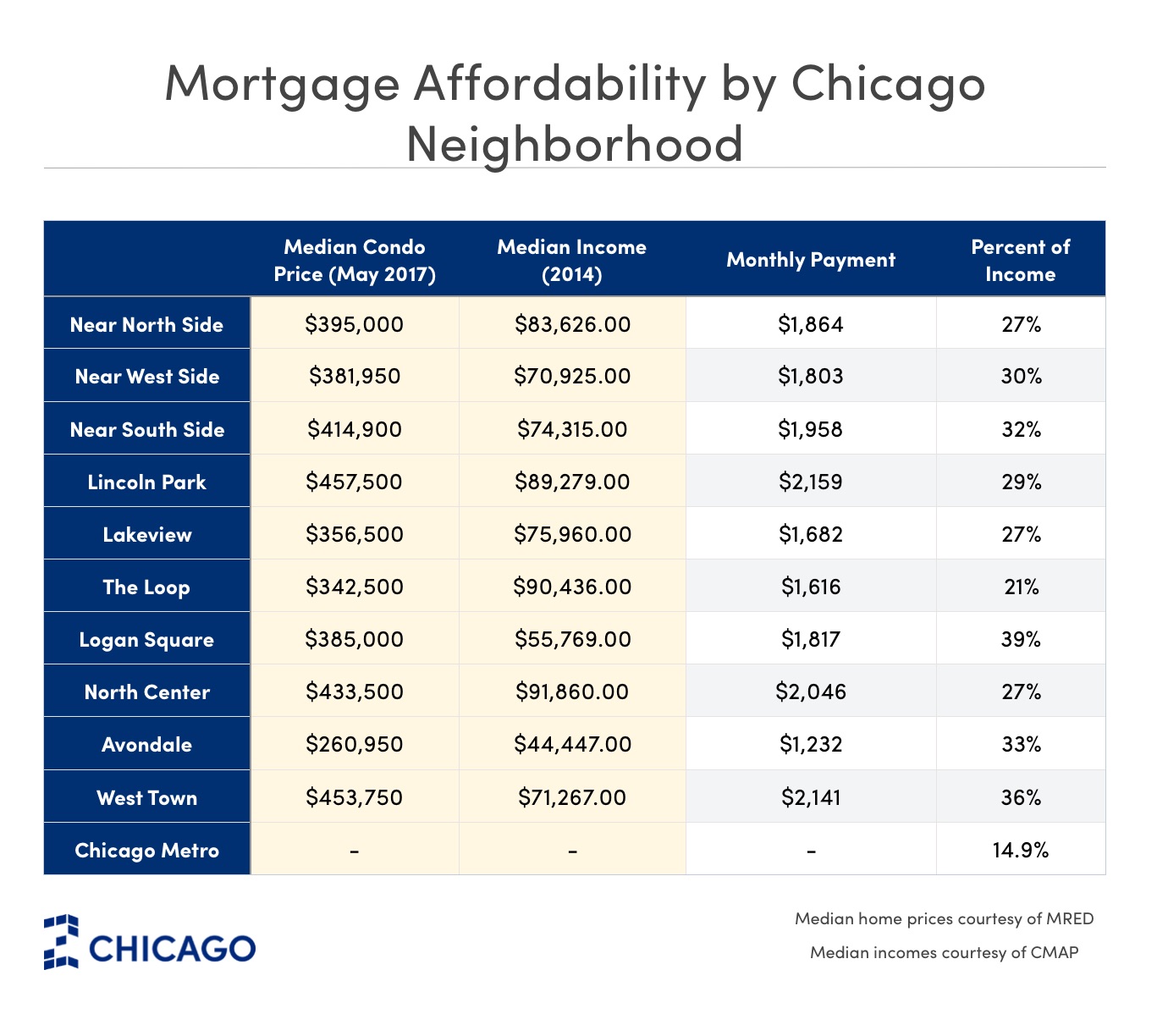

Chicago housing payments by neighborhood

If you’re one of the many Chicago renters considering homeownership, your first (understandable) concern is affordability. The good news is that once you overcome the down payment hurdle, mortgage payments are generally less expensive than comparable rent prices. Even so, homeownership affordability is entirely subjective. Your income and budget coupled with outside debts and general financial goals ultimately decide how much home you can afford.

According to Zillow, mortgage affordability in Chicago is 14.9 percent – that’s how much home buyers earning the metro area’s median income can expect to spend on their monthly mortgage payments. This makes Chicago metro homes more affordable, relative to income, than the national norm. Across the nation, home buyers earning median wages can expect to spend 15.9 percent of their income to pay off the median-priced home.

As you’ve probably guessed, Chicago home prices and median income levels vary substantially depending on the neighborhood. To break it down further, Z Chicago calculated how much neighborhood-specific mortgages cost (per month) as a percentage of that community’s respective median income.

Take Lincoln Park, where the median attached home (condo) price was 457,500, according to Midwest Real Estate Data’s (MRED) May 2017 report. A 30-year fixed mortgage on a condo at that price point equals $2,159 per month, including principal, interest and property taxes. Keep in mind, the monthly payment is projected assuming 20 percent down upfront ($91,500) and the current average 30-year fixed mortgage rate of 3.80 percent (Bankrate). When compared to the neighborhood’s median annual income of $89,279 (per CMAP), Lincoln Park homeowners spend about 29 percent of their paychecks on their mortgages.

Six out of 10 Chicago neighborhoods fall within the “30 percent rule,” which is the recommended percentage of income to spend on housing. Compared to San Francisco and New York City, where spending half (or more) of your income on rent or a mortgage is commonplace, even high-priced Chicago neighborhoods are reasonable. Since new wage data has yet to be released by the U.S. Census, it’s possible that some neighborhoods hold higher median incomes than the current estimates. This could potentially minimize the mortgage-to-income ratio in areas like West Town (Wicker Park), Avondale, Near South Side (South Loop) and Logan Square to fall at or below the suggested 30 percent ratio.

Call Z Chicago at 312-810-2295 when you’re ready to launch a personalized and practical Chicago home search. With your budget in mind, our team has the tools and proficiency to locate an ideal first, second or third home. From there, we’ll guide your home purchase process to ensure you make the most sensible investment with the best terms possible.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}